I’m asked a lot in money coaching – where do I start?

Of course, this question has a different answer depending on your answer to this question – where are you?

I can’t tell you where to start if I have no idea where you are today! Are you drowning in credit card debt? Or is your small business in trouble? Or are things generally good, but you are looking to maximize your investment returns?

Here’s the page I’ve tried my best to condense all my money advice into one easy to follow map, to guide you (no matter where you are) onto the path of money security and financial independence.

If you make it to the end of this map and need advice specific to your situation, shoot me an email and I’d love to chat.

Some general goals to shoot for:

- Make a spending plan and know where your money is going! (yes, the dreaded B word)

- Eliminate unnecessary expenses and prioritize spending goals

- 3-6 months of your expenses saved in the bank (this is called an Emergency Fund)

- Debt-freedom = no debt, and independence from borrowing/credit cards

- Enough savings to retire on (rule of thumb: 4%) invested in mutual funds

Now, some of those goals are HUGE and will take many years to accomplish. You may not be starting there, perhaps you have some smaller goals you need to do first. Maybe you need to get your bills current. Maybe you need to stop the cycle of payday lending, or save a tiny emergency fund to just get afloat.

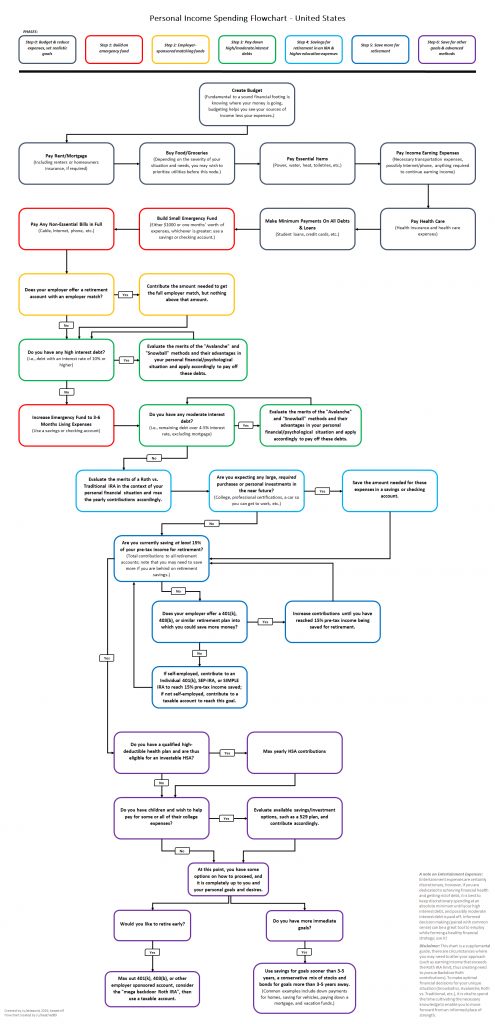

But what is the nitty gritty? What should I specifically do, and in what order? I’ve found a really nice flowchart made by a Reddit user to help you decide what to do with every dollar, in order by priority.

Click on the image or here to make it bigger.

I know it looks complicated (and hey, life is complex) but really it is just step by step. Once you have one of the boxes completed, you go to the next one.

Caveat: this is just for the basics of personal finance, and it is only the spending (outflow) portion of the equation (not the earning/income side). But it is extremely helpful as a guideline for where your money should be going.

Once again, this is very generic and I would love to help with your specific situation through one-on-one money coaching (first 30 minutes free!). You can change your life, and I can help.